When it comes to auto insurance, understanding the different types of coverage available can help you make better decisions about how to protect your vehicle. Two of the most common — and often confused — types of car insurance are comprehensive coverage and collision coverage. Both play an important role in protecting your financial well-being after an accident or unexpected event, but they serve different purposes.

In this detailed guide, we’ll explain what each type of coverage means, how they differ, when you need them, and how to decide which one is best for you.

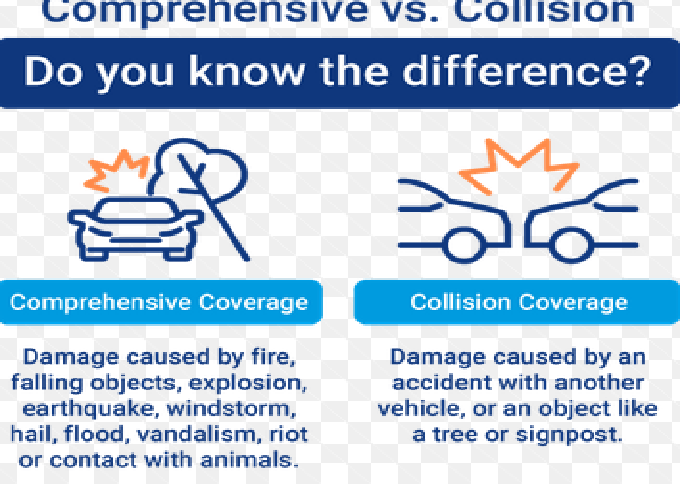

1. What Is Comprehensive Coverage?

Comprehensive coverage is designed to protect your vehicle from non-collision-related damages — in other words, incidents that do not involve another car or object on the road. It covers events that are often outside your control and not directly related to driving behavior.

Key Points About Comprehensive Coverage

-

It covers damages caused by theft, vandalism, fire, natural disasters, falling objects, and animal collisions.

-

It pays to repair or replace your car if it is damaged or destroyed by covered events.

-

It applies up to the actual cash value (ACV) of your car, minus your deductible.

-

Comprehensive coverage is optional in most states but may be required by lenders if you’re leasing or financing a vehicle.

Examples of Comprehensive Coverage in Action

-

Theft: If your car is stolen, comprehensive coverage helps pay to replace it.

-

Hail Damage: If a hailstorm dents your vehicle, comprehensive insurance covers repair costs.

-

Animal Collisions: If you hit a deer, comprehensive (not collision) pays for the damage.

-

Falling Objects: If a tree branch or debris falls on your parked car, it’s covered under comprehensive insurance.

-

Fire or Explosion: Damage from a vehicle fire or explosion is included.

Essentially, comprehensive insurance acts as a safety net for unpredictable events that can happen whether or not your car is being driven.

2. What Is Collision Coverage?

Collision coverage, on the other hand, covers damage to your car resulting from a collision with another vehicle or object, regardless of who is at fault. It’s designed to help you repair or replace your vehicle after an accident you cause or when the other driver’s insurance does not cover your loss.

Key Points About Collision Coverage

-

It covers damage from car accidents, rollovers, or collisions with stationary objects (like fences or poles).

-

It pays for repairs or replacement up to the vehicle’s actual cash value, minus your deductible.

-

It’s optional, but may be required by lenders if your vehicle is leased or financed.

Examples of Collision Coverage in Action

-

Accident with Another Car: If you hit another vehicle, your collision insurance covers your car’s repair costs.

-

Single-Car Accident: If you hit a tree, guardrail, or wall, collision coverage pays for the repairs.

-

Rollover Accident: If your vehicle rolls over after losing control, this coverage applies.

Collision coverage focuses on accidents you cause while driving, while comprehensive focuses on external factors and non-driving incidents.

3. The Main Difference Between Comprehensive and Collision Coverage

While both types of coverage help pay to repair or replace your car, the difference lies in how the damage occurs.

| Coverage Type | What It Covers | Examples |

|---|---|---|

| Comprehensive | Non-collision damage (external or natural causes) | Theft, fire, vandalism, hail, flood, hitting an animal, falling objects |

| Collision | Damage from vehicle accidents or collisions | Crashing into another car, hitting a pole, rolling over |

Think of it this way:

-

Comprehensive = “Acts of Nature or Misfortune.”

-

Collision = “Accidents You Cause While Driving.”

4. When Do You Need Comprehensive and Collision Coverage?

Although both are optional under most state laws, certain circumstances make them worthwhile — or even necessary.

You Should Consider Both If:

-

You have a new or high-value vehicle.

-

You’re leasing or financing your car (the lender will often require both).

-

You live in an area with a high risk of theft, vandalism, or natural disasters.

-

You want full protection regardless of fault or event type.

You Might Skip Them If:

-

Your car is old or low in market value (the cost of coverage might exceed potential benefits).

-

You can afford to replace your vehicle out of pocket if damaged or totaled.

-

You’re looking to reduce premium costs on an older vehicle.

It’s important to evaluate whether the annual cost of coverage plus your deductible makes financial sense compared to your car’s current value.

5. Deductibles and Claim Payments

Both comprehensive and collision coverage include a deductible, which is the amount you must pay before your insurer covers the rest.

For example:

-

Suppose your deductible is $500 and your car sustains $2,000 in damage.

-

You’ll pay $500, and your insurer will pay $1,500.

You can usually choose your deductible amount.

-

A higher deductible lowers your premium but increases out-of-pocket costs during a claim.

-

A lower deductible raises your premium but reduces what you pay in an accident.

6. How Insurance Companies Value Your Car

When filing a claim, your insurer won’t necessarily pay for a brand-new replacement car. Instead, they base the payout on your car’s Actual Cash Value (ACV) — its market value before the loss occurred, minus depreciation.

For example, if your car was worth $10,000 before an accident and your deductible is $1,000, the insurer would pay $9,000.

This means that for older cars with low ACV, comprehensive and collision coverage might not be worth the premium.

7. Cost Comparison Between Comprehensive and Collision Coverage

The cost of each coverage type varies depending on factors such as:

-

Your car’s make, model, and age.

-

Your driving history.

-

Where you live.

-

Your deductible amount.

-

Local claim statistics (e.g., theft or weather risk).

Generally:

-

Comprehensive coverage tends to be cheaper than collision.

-

Collision coverage is more expensive because it’s associated with more frequent and costly claims.

For instance, if comprehensive costs $200 annually and collision costs $400, adding both might total around $600 per year — but that’s still far less than paying for a new car out of pocket after a major incident.

8. Comprehensive and Collision Coverage in Practice

Let’s look at a few common scenarios to understand how these coverages apply:

Scenario 1: A Deer Hits Your Car

-

Coverage that applies: Comprehensive

-

Why: Animal collisions fall under non-driving incidents.

Scenario 2: You Rear-End Another Vehicle

-

Coverage that applies: Collision

-

Why: It’s a car-to-car accident caused by driving.

Scenario 3: Your Parked Car Gets Scratched by Vandalism

-

Coverage that applies: Comprehensive

-

Why: The damage happened while parked, not while driving.

Scenario 4: You Hit a Tree During Heavy Rain

-

Coverage that applies: Collision

-

Why: Even though the weather contributed, it’s still a driving collision.

Scenario 5: Your Car Is Damaged by a Falling Tree Branch

-

Coverage that applies: Comprehensive

-

Why: Falling objects are covered under comprehensive protection.

9. Is It Worth Having Both?

Many drivers choose to carry both comprehensive and collision coverage for full protection — commonly known as “full coverage” insurance (though technically, it doesn’t mean unlimited protection).

You should consider both if:

-

Your car is less than 8–10 years old.

-

Repair costs would be financially challenging without insurance.

-

You want peace of mind knowing you’re protected from both accidents and random events.

However, for older cars with lower value, you can calculate whether the premiums and deductibles justify the coverage. A simple formula helps:

If your annual comprehensive + collision premium exceeds 10% of your car’s value, consider dropping them.

10. Factors That Affect Whether You Need These Coverages

When deciding whether to purchase or drop comprehensive and collision coverage, consider these factors:

1. Vehicle Value

The newer and more expensive your car, the more sense it makes to have both coverages.

2. Location and Environment

-

High-crime areas or regions prone to flooding or storms increase the need for comprehensive insurance.

-

Urban areas with more traffic accidents might make collision coverage more useful.

3. Personal Finances

If paying for repairs or replacement out of pocket would strain your budget, these coverages can save you from financial stress.

4. Loan or Lease Terms

If your vehicle is financed or leased, your lender will likely require both types of coverage until the car is fully paid off.

5. Risk Tolerance

Some drivers prefer minimal insurance to save money. Others value peace of mind even if it costs more.

11. Common Myths About Comprehensive and Collision Coverage

Myth 1: Comprehensive Covers Everything

Despite its name, comprehensive doesn’t cover all damages — only non-collision events. You still need collision insurance for driving-related accidents.

Myth 2: Collision Covers Medical Bills

Collision only pays for damage to your car, not for injuries. Medical bills are covered under personal injury protection (PIP) or medical payments coverage (MedPay).

Myth 3: You Don’t Need Either if You’re a Good Driver

Even the safest drivers can’t control theft, natural disasters, or other drivers’ mistakes.

Myth 4: Your Insurance Will Always Replace Your Car

Insurance only pays up to the car’s actual cash value, not the price of a new car.

12. Tips to Lower Your Premiums

If you decide to keep both coverages but want to save money, here are a few strategies:

-

Increase Your Deductible: Choosing a higher deductible can reduce your monthly premium.

-

Bundle Insurance Policies: Combine auto and home insurance with one provider for a discount.

-

Install Safety Features: Anti-theft devices and dash cams can earn you discounts.

-

Maintain a Clean Driving Record: Fewer claims and tickets lower your rates.

-

Shop Around: Compare quotes from different insurers yearly.

-

Reassess Your Coverage: As your car ages, consider adjusting or removing coverage to save money.

13. Comprehensive vs. Collision: Which One Should You Prioritize?

If you can only afford one, your decision depends on the risks you face most often:

-

If you live in an area with high theft or severe weather, choose comprehensive.

-

If you drive frequently or in heavy traffic, collision may be more valuable.

Ideally, having both ensures well-rounded protection, but understanding your lifestyle and vehicle value helps prioritize smartly.

14. Conclusion: Understanding the Difference Saves You Money

Comprehensive and collision coverages are both valuable tools to protect your vehicle investment, but they cover very different risks.

-

Comprehensive handles unpredictable, non-driving events such as theft, vandalism, fire, or natural disasters.

-

Collision covers damages from car accidents or hitting objects while driving.

The right choice depends on your vehicle’s worth, driving habits, environment, and financial comfort level. For newer or financed cars, having both is highly recommended. For older vehicles, evaluate whether the cost outweighs the potential payout.

Ultimately, knowing the difference between comprehensive and collision coverage empowers you to make smarter, more cost-effective insurance decisions — and ensures that when the unexpected happens, you’re financially prepared.