Health insurance can often feel like a confusing maze of terms, numbers, and fine print. Words like “premium,” “deductible,” and “coverage” are commonly used, yet many people aren’t entirely sure what they mean or how they affect the cost and benefits of their insurance plan. Understanding these key concepts is essential to choosing the right health insurance policy, managing medical expenses, and ensuring that you are financially protected in case of unexpected health issues.

In this comprehensive guide, we will break down the most important health insurance terms — premiums, deductibles, copayments, coinsurance, and coverage — in simple language. We will also explore how these factors interact with each other and provide practical tips to help you make smart decisions when selecting or managing your health insurance plan.

1. What Is Health Insurance and Why It Matters

Health insurance is a contract between you (the policyholder) and an insurance company that helps cover the cost of medical expenses. In exchange for a regular payment called a premium, the insurance company agrees to pay a portion of your healthcare costs, such as doctor visits, hospital stays, surgeries, prescription drugs, and preventive care.

Without health insurance, medical costs can quickly become overwhelming. Even a short hospital stay or a minor surgery can cost thousands of dollars. Health insurance not only provides financial protection but also ensures access to quality healthcare services when you need them most.

2. Understanding the Basics of Health Insurance Plans

Before diving into specific terms, it’s helpful to understand how health insurance plans are structured. Most health insurance policies include:

-

Monthly Premium: The amount you pay regularly (usually every month) to keep your policy active.

-

Deductible: The amount you must pay out-of-pocket for medical expenses before your insurance begins to share the cost.

-

Copayment and Coinsurance: Your share of the cost for medical services after meeting your deductible.

-

Coverage: The range of healthcare services that your insurance plan will pay for.

-

Network: The group of doctors, hospitals, and clinics that have contracts with your insurance provider.

Each of these components plays a crucial role in determining how much you pay and what you receive from your health insurance plan.

3. Health Insurance Premiums Explained

A premium is the amount you pay to your health insurance company every month (or year) to keep your coverage active. Think of it as a subscription fee for your health insurance policy.

3.1 How Premiums Work

Paying your premium ensures that you remain enrolled in your plan and eligible for benefits. If you stop paying your premium, your coverage will eventually lapse, and you’ll have to pay for all medical costs out-of-pocket.

Premiums are usually due monthly, though some people choose to pay quarterly or annually depending on their plan’s terms.

3.2 Factors That Affect Premium Costs

Several factors determine the cost of your health insurance premium:

-

Age: Older individuals generally pay higher premiums because they tend to need more medical care.

-

Location: Healthcare costs vary by region, so where you live affects your premium.

-

Type of Plan: Comprehensive plans with more benefits tend to have higher premiums.

-

Coverage Level: Plans with lower deductibles and better coverage typically cost more.

-

Tobacco Use: Smokers or tobacco users often pay higher premiums.

-

Family Size: Covering more dependents increases the total premium amount.

3.3 Balancing Premiums and Other Costs

A common mistake is choosing a plan solely based on a low premium. While low-premium plans can save money upfront, they often come with higher deductibles and out-of-pocket costs when you need care. Conversely, higher-premium plans usually offer more comprehensive coverage and lower out-of-pocket expenses. The key is to find a balance based on your health needs and financial situation.

4. Understanding Deductibles

A deductible is the amount you must pay for covered healthcare services before your insurance company starts paying. For example, if your deductible is $1,500, you’ll need to pay the first $1,500 of your medical expenses yourself each year before your insurance begins to share costs.

4.1 How Deductibles Work

Once you meet your deductible, your insurance company starts covering a portion of your healthcare costs through copayments or coinsurance. However, preventive services such as vaccinations, annual checkups, and screenings are often covered without requiring you to pay the deductible.

4.2 High vs. Low Deductible Plans

-

High Deductible Plans: These usually come with lower premiums but higher out-of-pocket costs before insurance kicks in. They can be a good choice for healthy individuals who rarely need medical care.

-

Low Deductible Plans: These come with higher premiums but lower upfront costs when you need medical services. They are suitable for people with chronic conditions or frequent medical needs.

4.3 Deductibles and Out-of-Pocket Maximums

Your out-of-pocket maximum is the highest amount you’ll pay in a year for covered services. After you reach this limit, your insurance covers 100% of the remaining costs for the rest of the year. The deductible contributes toward this maximum, meaning every payment you make gets you closer to full coverage.

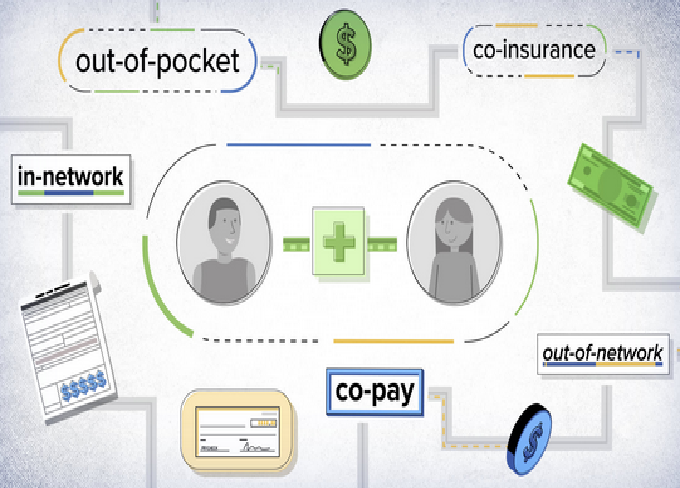

5. Copayments and Coinsurance

After meeting your deductible, you still may need to share costs with your insurance provider through copayments (copays) and coinsurance.

5.1 Copayments

A copayment is a fixed amount you pay for a covered healthcare service, such as $20 for a doctor visit or $10 for a prescription. Copays are predictable and make budgeting easier because you know in advance what you’ll pay for certain services.

5.2 Coinsurance

Coinsurance is the percentage of costs you share with your insurance company after meeting your deductible. For example, if your plan includes 20% coinsurance, you pay 20% of each medical bill, and your insurance covers 80%.

Coinsurance can vary depending on the service type — hospitalization, surgery, or specialist visits might have different rates.

5.3 The Relationship Between Deductibles, Copays, and Coinsurance

These three elements work together to determine how much you pay for medical care. Generally:

-

You pay the deductible first.

-

Then you pay copays or coinsurance.

-

Once you reach your out-of-pocket maximum, insurance covers everything.

6. What Is Coverage in Health Insurance?

Coverage refers to the range of medical services, treatments, and procedures that your insurance plan will pay for. Every plan specifies what is covered and what is excluded in the Summary of Benefits and Coverage (SBC).

6.1 Commonly Covered Services

Most comprehensive health insurance plans cover:

-

Doctor visits (general practitioners and specialists)

-

Hospital stays and surgeries

-

Prescription medications

-

Laboratory tests and imaging

-

Maternity and newborn care

-

Mental health and substance abuse treatment

-

Preventive care (vaccinations, screenings, wellness checkups)

-

Emergency services

6.2 Services That May Not Be Covered

Not all services are included in every policy. Common exclusions include:

-

Cosmetic surgeries

-

Dental and vision care (unless specified)

-

Experimental or unapproved treatments

-

Over-the-counter medications

-

Long-term care or private nursing

Before getting a procedure, it’s crucial to confirm whether your insurance plan covers it. Otherwise, you might be responsible for the full cost.

7. Understanding Provider Networks

Health insurance companies have agreements with specific doctors, hospitals, and clinics — collectively known as a provider network. The type of network you choose affects both your costs and the flexibility of your care.

7.1 In-Network vs. Out-of-Network

-

In-Network Providers: These are healthcare providers that have contracts with your insurance company to offer services at reduced rates. Visiting them saves you money.

-

Out-of-Network Providers: These providers are not contracted with your insurer, which usually means higher costs or no coverage at all.

7.2 Types of Network Plans

-

HMO (Health Maintenance Organization): Requires you to choose a primary care physician and get referrals for specialists. Coverage is limited to in-network providers.

-

PPO (Preferred Provider Organization): Offers more flexibility to see both in-network and out-of-network doctors without referrals.

-

EPO (Exclusive Provider Organization): Covers only in-network care but doesn’t require referrals.

-

POS (Point of Service): Combines elements of both HMO and PPO, allowing some out-of-network coverage.

8. Out-of-Pocket Costs and Maximum Limits

In addition to premiums and deductibles, health insurance includes other costs known as out-of-pocket expenses, which are the portions you pay directly.

8.1 Out-of-Pocket Maximum

This is the maximum you’ll pay in a policy year for covered services, including deductibles, copayments, and coinsurance. Once you hit this amount, your insurance covers 100% of the remaining costs.

8.2 Why the Out-of-Pocket Maximum Is Important

This limit provides a financial safety net, ensuring that even in the case of serious illness or injury, your medical bills won’t exceed a certain amount.

9. How Premiums, Deductibles, and Coverage Work Together

To understand how all these elements interact, let’s look at a practical example:

Suppose you have a plan with:

-

Monthly premium: $400

-

Annual deductible: $1,500

-

Coinsurance: 20%

-

Out-of-pocket maximum: $6,000

You visit the hospital for a $10,000 surgery:

-

You pay the first $1,500 (deductible).

-

Then, you pay 20% of the remaining $8,500 = $1,700 (coinsurance).

-

Your insurance covers the remaining $6,800.

-

Total cost to you: $3,200 for the year (not including monthly premiums).

This example illustrates how understanding your plan’s structure helps you anticipate costs and avoid financial surprises.

10. Choosing the Right Health Insurance Plan

Selecting the right plan depends on your health needs, budget, and risk tolerance.

10.1 For Young, Healthy Individuals

A high-deductible, low-premium plan might be ideal. It keeps monthly costs low while protecting against major medical emergencies.

10.2 For Families

A moderate plan with balanced premiums and deductibles ensures coverage for children’s healthcare and unexpected family medical needs.

10.3 For Individuals with Chronic Conditions

A low-deductible plan with higher premiums may be better since you’re likely to need frequent medical care throughout the year.

11. Tips for Managing Health Insurance Costs

Here are some practical ways to save money while maintaining good coverage:

-

Use preventive care benefits: Many preventive services are fully covered, helping you avoid costly conditions later.

-

Stay in-network: Always use in-network providers to minimize out-of-pocket costs.

-

Compare plans annually: Health insurance options and prices change every year, so review your plan during open enrollment.

-

Consider an HSA (Health Savings Account): If you have a high-deductible plan, an HSA lets you save tax-free money for medical expenses.

-

Avoid unnecessary emergency room visits: Use urgent care centers for non-emergency issues to save money.

12. Common Mistakes to Avoid

When dealing with health insurance, it’s easy to make costly mistakes. Avoid these pitfalls:

-

Ignoring the deductible: Don’t focus only on premiums; consider how much you’ll pay before coverage begins.

-

Assuming all services are covered: Always read your policy details carefully.

-

Not checking network providers: Visiting an out-of-network doctor can result in unexpectedly high bills.

-

Skipping preventive care: Regular checkups can prevent serious health issues and reduce costs long-term.

13. The Importance of Understanding Your Plan

Many people only learn about their health insurance details when a medical emergency happens — and by then, it’s too late to make changes. Taking the time to understand how premiums, deductibles, and coverage work can save you money and stress. Being informed helps you:

-

Choose a plan that fits your lifestyle and health needs.

-

Avoid financial shocks from unexpected medical bills.

-

Maximize the value of your insurance benefits.

Conclusion

Health insurance doesn’t have to be confusing once you understand the key terms. Premiums are what you pay to keep your plan active, deductibles are what you pay before coverage starts, and coverage determines what services your insurer will pay for. Each of these elements influences your total healthcare costs and your level of financial protection.

By learning how these factors work together, you can make smarter decisions, choose the right health insurance plan, and manage your healthcare expenses effectively. Ultimately, health insurance is not just a legal or financial requirement — it’s an investment in your health, peace of mind, and future well-being.